Collectible Card Games Market Overview

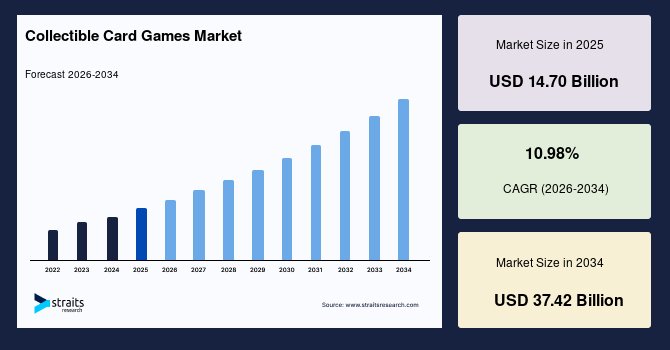

The global collectible card games market size was estimated at USD 14.70 billion in 2025 and is projected to reach from USD 16.26 billion in 2026 to USD 37.42 billion by 2034, growing at a CAGR of 10.98% during the forecast period (2026-2034). The growth of the market is attributed to digital transformation and mobile gaming adoption and E-commerce and distribution growth

Key Market Trends & Insights

- North America held a dominant share of the global market with a market share of 46% in 2025.

- The Asia Pacific region is growing at the fastest pace, with a CAGR of 12.5%.

- The U.S. dominates the CCG market in 2025.

Market Size & Forecast

- 2025 Market Size: USD 14.70 billion

- 2034 Projected Market Size: USD 37.42 billion

- CAGR (2026-2034): 10.98%

- Dominating Region: North America

- Fastest-Growing Region: Asia Pacific

The global collectible card games market growth is attributed to the simultaneous expansion of flagship franchises and premium licensed releases, digital CCG ecosystems like MTG Arena and Hearthstone that funnel players to physical play, and rapidly growing secondary and e-commerce marketplaces that increase liquidity and collector interest.

The CCG market combines physical collectible product sales like booster packs, sealed sets, special editions, and digital card-game ecosystems. The market is characterised by blockbuster licensed releases like high-profile Magic sets and continued Pokémon print runs, renewed digital engagement, and stronger marketplace infrastructure. The expansion of e-commerce and marketplace consolidation improves access and price discovery for rare cards, attracting both hobbyists and investors.

Collectible Card Games Market Trends

Growing popularity of TCGs among youth and adults

Trading card games (TCGs) have become more popular across all age groups. Kids play them in schools and after school clubs, college students join campus leagues, and adults collect or play both for fun and investment. Publishers are keeping up with demand by releasing more sets, licensed tie-ins, and premium products.

- For instance, the Pokémon Company’s report shows 10.2 billion cards produced between March 2024 and March 2025, reflecting significant market presence.

Furthermore, local game stores, live events, and streaming platforms like Twitch and YouTube help attract new players, keeping sales strong and promoting market growth.

Rising collector culture

The rise in collector culture drives the market. High-profile card auctions and rare pulls attract media attention, drawing in both fans and investors. This fuels demand for premium boxes, limited sets, and special “chase” cards. Collectors often spend more than casual players, and services like grading and auctions make it easier to buy and sell high-value cards. Publishers respond with chase mechanics, premium bundles, and limited runs designed to capture collector spend.

Collectible Card Games Market Growth Factors

Digital transformation and mobile gaming adoption

Digital platforms like MTG Arena and Hearthstone are becoming equally important as physical cards. They make it easier for new players to start playing, allow fans to test decks before tournaments, and create new revenue streams through digital packs and cosmetics. Online tournaments also help fill the gap between physical set launches.

- For instance, in August 2025, MTG Arena announced the release of “Alchemy: Edge of Eternities”. This digital-only set features 39 new cards and is available through MTG Arena-exclusive formats.

While some players may spend more digitally than on physical cards, these platforms expand the overall ecosystem and increase long-term engagement.

E-commerce and distribution growth

The expansion of e-commerce platforms like eBay and TCGplayer has transformed the way people buy and sell cards. Collectors and players have global access to sealed products, singles, and graded items, while publishers can reach more markets without relying on physical stores. These platforms also make it easier to resell cards, giving collectors more confidence to invest in rare items. This has expanded the overall availability and presence of the market.

Market Restraint

Counterfeit and grey-market cards

The growth in secondary markets raises the risk of counterfeit cards and grey-market imports, with fraud incidents and authenticity concerns eroding buyer confidence. High-value auction lanes and online marketplaces have led to increased scrutiny and occasional platform disputes. Even though platform consolidation helps in large marketplaces with fraud-prevention resources, smaller sellers and informal channels remain vulnerable. Overall, with cases of marketplace friction and brand reputation rising, the operational risks of a high-value secondary market are increasing.

Market Opportunity

Expanding secondary markets and services for collectors

The rise of secondary markets such as auction houses, grading services, and global online platforms has opened new revenue opportunities for the collectible card games market. Publishers can monetize from the resale market through official grading partnerships, buyback programs, and consignment services. Platforms like eBay’s integration with TCGplayer and Fanatics’ expansion into trading cards have made it easier for collectors to buy and sell, which keeps the market active instead of cards just sitting in collections. With record-breaking auctions and strong Pokémon demand, the secondary market is becoming an essential growth area for publishers and marketplaces alike.

- 📊 Preview Report Scope and Structure – Gain immediate visibility into key topics, market segments, and data frameworks covered.

- 📥 Evaluate Strategic Insights – Access selected charts, statistics, and analyst-driven commentary derived from the final report deliverables.

Regional Analysis

North America remains the clear leader in the global CCG market, holding a revenue share of 46% in 2025, with unmatched revenue, infrastructure, and organized play. The region’s mature retail ecosystem, spanning specialty shops, big-box launches, and strong online platforms, makes it easy for players to buy in. High disposable incomes and vibrant content communities on Twitch and YouTube further amplify discovery and engagement. North America also hosts the deepest secondary-market infrastructure, with grading services, auction houses, and platforms like eBay/TCGplayer consolidating liquidity. Together, these factors cement North America’s role as the commercial and cultural hub of the CCG world.

The U.S. is the world’s largest and most commercially developed CCG market. It combines publisher headquarters, expansive retail footprints, and the deepest tournament ecosystem with the strongest liquidity in secondary markets. U.S. retailers create wide distribution coverage, while e-commerce leaders like eBay and TCGplayer streamline preorders, singles trading, and global resale. Hobby conventions and sanctioned tournament series bring recurring spikes in demand and drive community growth.

Canada represents a smaller but valuable market, supported by organized play circuits, strong specialty-store networks, and seamless cross-border flows with the U.S. Canadian players actively participate in global publisher programs such as prereleases and qualifiers, while local conventions help sustain community engagement. Consumer demand mirrors U.S. trends, with strong interest in Magic, Pokémon, and Yu-Gi-Oh!, backed by steady sealed-product sales and growing activity on secondary-market platforms like eBay/TCGplayer.

Asia Pacific Collectible Card Games Market Trends

Asia-Pacific, led by Japan, China, and Southeast Asia, is the fastest-growing region for CCGs, blending mass market appeal with an emerging collector culture. Japan continues to anchor the market as both Pokémon’s home and a mature hub for collectors. China, meanwhile, is experiencing rapid expansion, driven by retail growth, a rising middle class, and accelerating organized play scenes. Southeast Asia adds momentum through strong youth adoption and grassroots tournament networks. Mobile and digital crossovers, such as Pokémon TCG Pocket, are lowering entry barriers and introducing new demographics. Combined with Asia’s booming e-commerce penetration, these dynamics make APAC the standout growth engine of the global market.

China has quickly become one of the fastest-growing CCG markets, especially for mainstream IPs like Pokémon. Following localized launches, demand has surged across retail and online ecosystems, with major e-commerce platforms making products widely available and fueling collector speculation. Organized play and tournaments are gaining momentum, while mobile and digital integrations help lower entry barriers and broaden participation.

Europe Collectible Card Games Market Trends

The UK is a key Western European market, supported by a robust local game store network, frequent large-scale tournaments, and reliable distribution channels. Retailers host prereleases and sealed-product launches that create repeat demand cycles, while the country’s established e-commerce infrastructure enables synchronized releases with other European markets. The UK continues to be a favored test market for limited releases and special SKUs before wider European rollouts, underlining its importance as both a commercial hub and trendsetter in Europe.

Germany is one of Europe’s strongest CCG markets, with a deep-rooted board game culture and extensive organized play. National championships, regional tournaments, and fan conventions are well-attended, and publishers routinely localize products into German editions to support demand. Its central location and advanced logistics infrastructure make Germany a distribution hub for much of Europe, serving both retail and secondary-market fulfillment. For collectors and competitive players alike, Germany offers a steady flow of supply, demand, and community engagement, reinforcing its role as a cornerstone of Europe’s CCG market.

Market Segmentation

Device Type Insights

Physical product sales remain the backbone of the CCG market, with booster packs as the single biggest driver of sales. Publishers design a steady cadence of core sets, expansions, and special drops to keep players returning to stores, fueling both casual play and collector speculation. Boosters create foot traffic, power pre-release events, and underpin secondary-market value through rare pulls.

Age Type Insights

Adults dominate the market in both spending and participation. Wizards’ surveys show many players in their late 20s–30s, with a third having over a decade of experience, underscoring long-term engagement. Organized play, from MagicCon to regional Pokémon events, skews heavily adult, while mobile ecosystems like Pokémon GO draw 21–30 year-olds into both digital and tabletop products. Adults drive premium demand, sealed cases, collector editions, and graded singles, and their discretionary income powers both high-value auctions and everyday event spend.

Card Type Insights

Character cards dominate the market, defining gameplay, shaping the metagame, and commanding the highest values on secondary markets. These are the cards players build decks around, collectors chase, and publishers spotlight in marketing. Rare or legendary characters often anchor booster-set value, and their scarcity fuels excitement and speculation. Their cultural impact extends to licensed characters from films, anime, or games, which usually drive crossover sales and expand audiences.

Game Type Insights

Strategy-driven titles such as Magic: The Gathering and Yu-Gi-Oh! dominate the market by combining complex gameplay, robust tournament circuits, and recurring purchases. These games foster deep commitment; players continually invest in new sets to keep up with evolving metas. This model creates exceptionally high lifetime value per player, as purchases extend beyond boosters to premium sealed products, tournament entry, and digital versions like MTG Arena.

Distribution Channel Insights

Online Retail dominates the market. E-commerce has overtaken traditional distribution in scale and reach, with platforms like eBay (via TCGplayer) and Fanatics Collect (via PWCC acquisition) consolidating trading infrastructure. Online marketplaces give publishers global distribution, collectors fast liquidity, and retailers expanded audiences. This visibility supports speculative buying, since players know they can resell singles and sealed products easily.

Revenue Model Insights

Direct physical sales remain the primary revenue engine. Every set launch generates predictable cash flow through booster packs, specialty boxes, and prerelease sealed product. Hasbro and Pokémon’s financials confirm that physical sales remain central, with Pokémon’s 10.2 billion cards printed in FY 2024–25 as proof of enduring scale. Premium bundles and collector editions drive margin expansion, while digital platforms complement rather than replace physical sales, serving as funnels that sustain tabletop engagement.

Player Type Insights

Casual players form the largest share of the community, sustaining steady sealed sales and local play environments. They are the discovery engine, ensuring new players keep entering the hobby. Record-setting auction prices for rare singles both validate collector demand and drive cultural visibility, encouraging casuals to participate more deeply. Publishers balance content-accessible play experiences for casuals and limited premium products for collectors, ensuring broad participation and a high margin of upside.

Competitive Landscape

The market is moderately fragmented, with major publishers and platforms following three commercial patterns. IP-first publishers focus on frequent set cadence, premium limited SKUs, and organized-play ecosystems. Regional and licensed target local markets and sports/entertainment tie-ins. Platform and service players like eBay, Fanatics Collect supply marketplace liquidity, grading, and custodial services.

Wizards of the Coast (Hasbro) – An emerging player: Wizards (Hasbro) monetizes via a multi-channel model: core set releases and premium boxed products, organized-play circuits, digital conversion (MTG Arena), and licensed crossovers. Wizards’ model balances high-cadence retail consumption with collector premium SKUs that generate secondary-market interest.

Latest news:

- In July 2025, Hasbro’s Wizards of the Coast segment showed continued strength in Q2 2025, with Magic: The Gathering revenue up 23%, driven by the record-breaking success of the Final Fantasy set release.

List of key players in Collectible Card Games Market

- Wizards of the Coast (Hasbro)

- The Pokémon Company

- Konami (Yu-Gi-Oh!)

- Bandai / Bandai Namco

- Bushiroad

- Panini

- Upper Deck

- Blizzard/Activision (Hearthstone digital)

- Fantasy Flight / Asmodee

- Cygames (Shadowverse)

- NetEase

- eBay/TCGplayer

- Fanatics (PWCC/Fanatics Collect)

- Cardmarket (Europe)

Recent Developments

- In August 2025, Konami hosted the Yu-Gi-Oh! World Championship (WCS) 2025 finals in Paris. It was the culmination of the 2025 season, with new champions crowned in the Yu-Gi-Oh! Trading Card Game, Duel Links, and Master Duel.

- In July 2025, Bandai Namco launched the Gundam Card Game, with four starter decks released globally. A new set, Newtype Rising [GD01], was also released.

Collectible Card Games Market Segmentations

By Device Type (2022-2034)

-

Physical Cards

- Booster Packs

- Starter Decks

- Collector / Premium Editions

- Digital / Online

- Hybrid Platforms

By Age Type (2022-2034)

- Children

- Teenagers

- Adults

By Card Type (2022-2034)

- Character Card

- Autograph Card

- Image Card

- Ability Cards

- Others

By Game Type (2022-2034)

- Strategy-Based

- Collectible-Focused

- Casual / Social

By Distribution Channel (2022-2034)

-

Offline Retail

- Specialty Game Stores

- Toy / Department Stores

- Tournament / Event Sales

-

Online Retail

- Brand Websites

- E-commerce Marketplaces

By Revenue Model (2022-2034)

- Direct Sales

- Subscription / Digital Packs

- In-App Purchases

- Tournament / Event Fees

Player Type (2022-2034)

- Casual Players

- Competitive Players

- Collectors / Investors

By Region (2022-2034)

-

North America

- U.S.

- Canada

-

Europe

- U.K.

- Germany

- France

- Spain

- Italy

- Russia

- Nordic

- Benelux

- Rest of Europe

-

APAC

- China

- Korea

- Japan

- India

- Australia

- Singapore

- Taiwan

- South East Asia

- Rest of Asia-Pacific

-

Middle East and Africa

- UAE

- Turkey

- Saudi Arabia

- South Africa

- Egypt

- Nigeria

- Rest of MEA

-

LATAM

- Brazil

- Mexico

- Argentina

- Chile

- Colombia

- Rest of LATAM

Frequently Asked Questions (FAQs)

The global collectible card games market size was estimated at USD 14.70 billion in 2025 and is projected to reach from USD 16.26 billion in 2026 to USD 37.42 billion by 2034, growing at a CAGR of 10.98% during the forecast period (2026-2034).